Loan application and it’s underwriting processes are a practice of analysing, structuring, documenting, and approving credits. Therefore, to achieve all these, lenders need tools to guide them through the process. Also, while considering the risk in credit and following the fact, it is relevant to emphasize on the need to protect financial institutions and individual lenders, hence the five Cs of credit. The 5Cs are fundamental tenets of lending loans.

With the result of the recent CGAP in Kenya, it was noticed that 50% of digital borrowers repay their loan late and default, respectively. To investigate and describe the creditworthiness analysis methods, strategies and procedures, they form requirements within the analysing process.

Thus, let us discuss the 5Cs of credit and all you need to know.

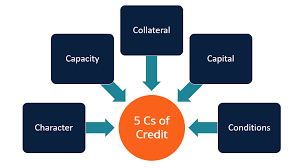

What are Five C’s of credit?

The five Cs of credit are a gauge or a system used in weighing creditworthiness of borrowers. It gauges five features of the borrowers, which are capacity, character, capital, collateral, and conditions. Moreso, it analyzes the probability of loan default and capacity for repayment.

No five Cs are more important than the other, but most lenders gauge using capacity. The goal is your ability and willingness to repay your loan.

Understanding the five C’s of credit in Kenya

The 5Cs of credit in Kenya have to do with a series of credit analysis by a lender to find out the risk associated with a loan. Regardless of the type of loan you need, the lender is interested in how you will pay back the loan.

In Kenya, credit analysis is governed and controlled by the “five Cs”. The borrower’s character, capacity, condition, capital, and collateral. These 5 components make up the credit analysis. It also helps the lender understand you as a borrower and your creditworthiness.

Finally, it is pertinent as a Kenya citizen that you understand these five Cs . It would prepare you for a loan application process and give you the edge you need.

Five C’s of credit in Kenya

In gauging creditworthiness of potential borrowers, 5 features of five Cs are considered. They are:

- Character/credit history

- Capacity

- Collateral

- Capital

- Conditions

Character/credit history

This refers to the borrower’s repayment track records. Reputation appears in your credit history. It is generated by the CRB in Kenya and contains how much you borrowed and your loan defaults and repayments. Often, if you are looking for jobs, you might be asked to get your credit certificate.

Many lenders also gave a minimum credit score and requirements before a borrower is eligible. Also note that a low interest rate is offered to borrowers with an excellent credit score.

Capacity

This is the ability of the borrower to repay the loan. It is often assessed based on the borrower’s debt-income ratio. They obtained it by adding the potential borrower’s monthly debts payment and dividing it by the gross salary or income.

The lower the DTI, the higher the chance. The length of hon and the job stability are also considered as part of the capacity of the borrower.

Collateral

Collateral prices, the risk of loan. They presented it in exchange for loans. It assures the lender that he can get something back in case of default. It is the object of the loan application.

They also referred to as secured loans. Loans secured with collateral often have low interest rates and longer loan duration such as with mortgage loans providers.

Capital

This includes the down payment of loans to show more seriousness and willingness to repay loans. This down payment can make lenders comfortable in extending the loan. A large capital by the borrower reduces the risk of default.

Conditions

This includes the conditions for the loan, the principal amount, and the interest rate the loan would attract. This also explains what the borrower is using the loan for.

These are the things the lenders find out. The reason behind every loan influences lenders’ decisions for approval.

Basics of five C’s of credit

The five-Cs-of-credit methods and evaluation are rooted on;

- Qualitative and

- Quantitative measures.

Lenders approve and grant loan applications based on borrower’s credit reports, credit scores, income statements, and other documents. Documents relevant to the borrower’s financial situation are the only one considered. Take note that the information about the loan itself is also considered.

How lenders analyse the five C’s of credit

Different lenders analyse it differently based on how they want it. They can use any of the 5Cs as a basic gauge for analysis. Let us quickly look at the 5Cs and see how lenders analyse it.

Character: Lenders look at:

- Credit score/history

- Financial reputation

- Other financial credit utilisation

Capacity: Lenders analyse it by looking at:

- Cash flow

- Debt-to-income ratio

- Debt service ratio

Capital Lenders will want to see:

- How much you have invested in your business

- Your business net worth

- The real estate you possess

- Ratio of your debt to equity

- The equipment and assets you have

Collateral: Financial institution can perceive it in the form of:

- Your Valuable assets

- Depreciation rates of your assets

- Account receivables

Conditions: conditions include other factors that will influence your loan repayments. They are:

- Economic trends

- Issues that are predominant in your business or your workplace

- Tangible reasons for the loan application.

Why are Five C’s of credit important

The importance of five C’s of credit are:

- important?It helps lenders determine the borrower’s credit limit and the interest rate.

- It influences, to a large extent, the borrower’s loan approval.

- The 5Cs, when properly analysed, give the lender conditions that the borrower would pay back.

How to improve on the five C’s of credit by a borrower

Improving on the 5Cs of credit by the lender involves distinct steps. They include:

- Make your payments early

- Create a mutual relationship with lenders

- Reduce your debts by clearing outstanding debts

- Increase your cash flow

- Record all your personal investments and knowing off hand

- Gain and purchase assets

- Control the way you sound. Prepare yourself and use all your loans prudently.

Frequently asked questions

Of importance, let us recap. The 5 C’s of credit are Character, Capacity, Collateral, Capital, and Conditions.

Why are they all important?

Lenders use these criteria to know if you are qualified for a loan. Eligibility is first considered before a loan application process.

These criteria determine your interest rates and credit limits. They also help determine loan risk and the likelihood of the borrower repaying at the agreed date.

Is there a sixth ‘C’ of credit?

Often people refer to the credit report/history as the 6th C of credit. It is not yet verified.

Conclusion

Each financial institution has its own method for analyzing a borrower’s creditworthiness. Using the five Cs of credit is common for both individual and business loan applications.

Of hierarchy, capacity basically, the borrower’s ability to generate consistent income to pay off the interest and principal ranks as the most important.

But applicants who have high marks in each category are more apt to receive bigger loans, a lower interest rate, and more favorable repayment terms.

These factors are what lenders used to gauge your creditworthiness, but make no mistake. It’s also important for the financial health and stability of your business to check the 5 Cs of credit analysis on your own from time to time. Whether for lenders or for yourself, use this guide to help you strengthen your business’s 5 Cs of credit!